Anna Gelpern is a professor at Georgetown Law, and a non-resident fellow at the Peterson Institute for International Economics.

Unscrupulous rulers can ignore court orders, hoard gold bars while snubbing their creditors, and if all else fails, rewrite the rules. Why, then, does everyone keep lending them more and more money?

Even before Argentina’s latest bid to donate its body to sovereign debt learning, FTAlphaville spent over a decade documenting investors’ quest to overcome sovereign debt defences. A few succeed beyond measure. Is their secret luck? Overwhelming force? A knack for concocting novel legal theories?

Investigative reporting and academic research all point to a practical hack — flow control.

Few rulers can survive for long cut off from international payment flows. A creditor that can block or capture some of these flows therefore gains a source of repayment, an information advantage, and bargaining leverage against the debtor and, crucially, against other creditors. London bankers in the 1800s, diplomat-debt collectors in the early 1900s, commercial banks and export credit agencies in the 1990s, and distressed debt funds and commodity traders in the 2000s have all deployed this insight to their advantage when extending credit to governments around the world.

Chinese creditors have in recent decades ventured into risky sovereign lending at scale, and in the process they have expanded and adapted what might be the most robust model yet of sovereign cash flow control.

A new working paper and companion essay (co-authored with Omar Haddad, Sebastian Horn, Paulina Kintzinger, Bradley Parks, Christoph Trebesch) document a remarkable pattern of secured lending by Chinese institutions to low and middle-income countries between 2000 and 2021.

Leading academic theories start from the premise that the role of collateral in sovereign debt repayment is “negligible”, but it turns out that the reality disagrees. Nearly half of all Chinese lending commitments over the past 20 years (a whopping $420bn in constant 2021 US dollars) were backed by cash flows, bank deposits, or on very rare occasion, by physical assets.

Contrary to popular political narratives, it turns out that Chinese banks hardly ever take real estate or goods as collateral, and we have seen no ports or railroads in hock to Belt and Road.

Instead, Chinese lenders appear to seek reliable, observable, accessible, and liquid assets, as close as possible to cash collateral. Foreign currency revenues routed through creditor-controlled bank accounts backed 79 per cent of the lending volume. The account was often at the creditor bank, which could monitor the cash flows, limit withdrawals, and set off unpaid debts against the account balance.

These findings corroborate recent claims by the IMF and the World Bank that secured sovereign debt was on the rise. Yet heavily indebted, commodity-exporting, low-income countries with infinite unmet needs for money and known governance challenges are particularly prone to giving foreign — in this case, Chinese — creditors control over hard currency cash flows.

In fact, we can see a clear pattern of vulnerable governments using established commodity export revenues as collateral for unrelated and risky domestic infrastructure projects.

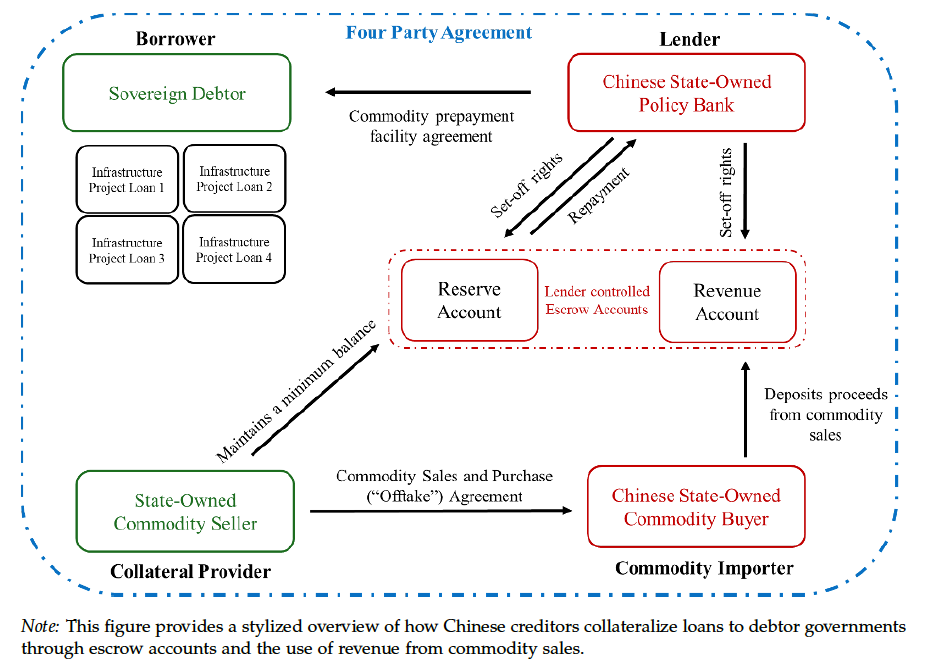

Here’s how it works: The borrower’s state-owned commodity exporter typically directs its Chinese buyer to route its payments directly into creditor-controlled bank accounts. The accounts would be used to pay Chinese engineering and construction companies building the infrastructure, then to pay the debt, and last of all, would find their way to the exporter’s state treasury.

In this arrangement, exporters whose steady earnings pay for the infrastructure may see no direct benefit from it. Meanwhile, infrastructure builders and operators rely on exporters to repay project debts, and might have zero incentive to manage their risks. This is quite unlike conventional export or project finance, where creditors’ repayment depends on the performance of the project itself.

Here’s a stylised example (zoomable version):

Taken together, these secured lending practices create large, ringfenced revenue streams from vulnerable countries to offshore bank accounts. These foreign currency cash flows remain frozen and out of public sight — sometimes for many years. In the riskier, more precarious countries with available data, revenues stuck in these bank accounts average at more than 20 per cent of annual external public debt service.

Ringfenced revenues are not available for other government expenditures, nor for payments to other creditors. They can therefore severely limit countries’ fiscal space and autonomy, and raise doubts about the usefulness of fiscal monitoring in countries that rely on this collateralisation mechanism.

Sure, flow control was a feature of sovereign borrowing for years before Chinese institutions scaled up their lending, and is not unique to them. But how big is this iceberg? Who knows!

This opacity is a central challenge. It’s difficult to assess whether and how debtors, creditors or the public benefit from these collateral arrangements. The thicket of interlocking debt, sales, security, and construction contracts — implicating multiple institutions in China and the borrowing country — makes it impossible to gauge the costs or benefits of any given aspect of the relationship.

Although some of the restricted bank accounts accrue interest, rates are rarely disclosed. Some contracts are awkwardly drafted; renegotiation and enforcement take place out of the public eye. Public information about encumbered cash flows is limited, fragmented, and contested.

Cross-collateralisation, cash collateral pooling, and other complex and layered structures are familiar tools, but can obscure fragility, transmit risks in unpredictable ways, and make it harder to manage debt distress. It should go without saying that they make a mockery of negative pledge clauses in sovereign debt contracts. Poorly designed secured transactions harm lenders, borrowers, and the development finance system.

In sum, giving one particular creditor effective control over government cash flows radically alters the debtor-creditor and inter-creditor power balance. However, when traditional development aid is retreat, it might be the only way to build essential public infrastructure in vulnerable countries. It might explain why even the riskiest borrowers sometimes borrow abroad. Puzzle solved, but there’s little comfort in this solution.

When every creditor must assume that someone else is taking collateral, policymakers would do well to prepare for a collateral arms race and a 19th century-style grab race to follow.

Source link

{kind=link}

{kind=link}