In a world where economic headlines shift as quickly as the weather, keeping tabs on consumer sentiment and retail sales feels like a full-time job. But for individuals juggling budgets, small business owners stocking shelves, or large enterprises plotting strategies, these aren’t just numbers—they’re lifelines.

Here at Market World, we cut through the noise to deliver economic news that matters. Whether you’re watching how U.S. trends affect global markets or you are a local business owner, this guide explains the pulse of the American economy in 2025.

Why do these numbers matter?

- Consumer Sentiment: Think of this as a crystal ball. It signals how Americans feel about their wallets. When confidence dips, spending usually slows down soon after.

- Retail Sales: This is the engine of the economy. Spending drives about 70% of U.S. growth.

In 2025, this duo has been under pressure. We are facing rising borrowing costs, stubborn inflation (prices that won’t come down), a cooling job market, and global trade issues. Consumers are more cautious than ever. They are pinching pennies on luxuries and focusing only on essentials.

Why track these quarterly?

- Businesses: To spot trends early for smarter inventory and pricing.

- Individuals: To decide when to make big purchases like homes or cars.

- Enterprises: To forecast demand that could make or break their year.

Looking back at Q4 2024 versus Q4 2025, we’ve seen a shift. Last year, optimism sparked a 4.2% jump in retail sales. Fast-forward to 2025, and sentiment has dropped near record lows. Retail growth has slowed to 3.9%.

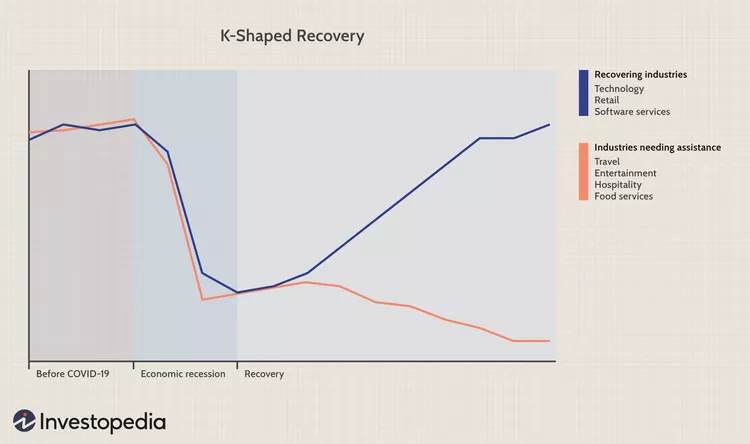

Holiday spending held up online but dropped in physical stores. This revealed a “K-shaped” recovery—high earners are still spending, while everyone else is holding back.

Understanding Consumer Sentiment: Is Confidence Rising or Falling in 2025?

Consumer confidence isn’t just a buzzword—it is the pulse of the U.S. economy. We measure this through surveys like the University of Michigan Consumer Sentiment Index and the Conference Board’s Consumer Confidence Index. These surveys ask people how they feel about their finances and jobs.

In 2025, the story is one of decline:

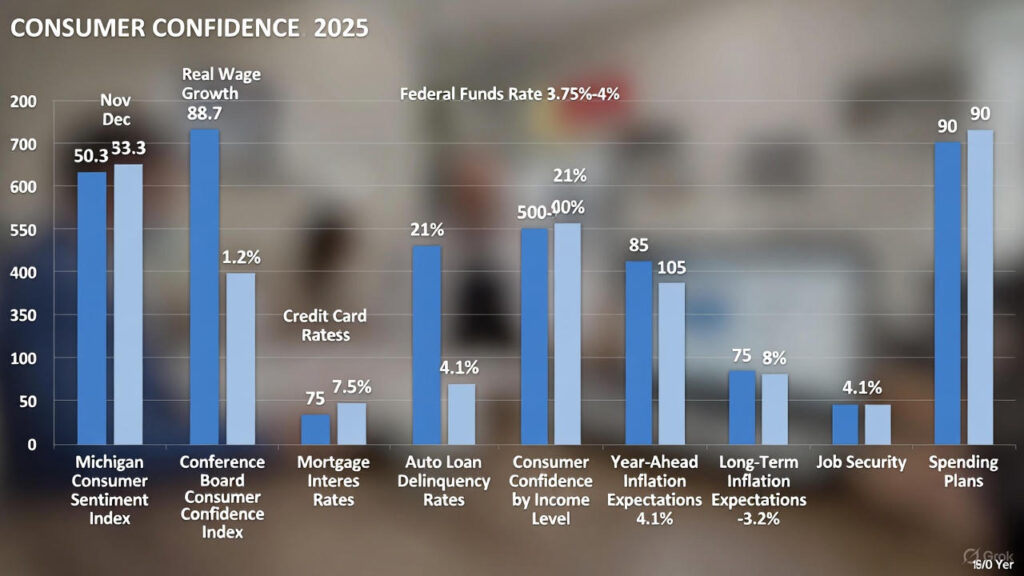

- The Michigan index plunged to 50.3 in November (its second-lowest ever) before a slight bump to 53.3 in December.

- The Conference Board hit 88.7 in November, the lowest since April.

Both are down sharply from 2024 averages. This signals that people are worried.

Is confidence higher than last year? Not even close. It has fallen 20-30% across the board. This drop was fueled by three main factors:

- Political Instability: A federal shutdown disrupted benefits and flights, making people nervous.

- Shrinking Purchasing Power: Wages grew by 1.2%, but inflation (prices) grew by 3%. This means consumers feel poorer than before.

- High Borrowing Costs: The Fed funds rate (3.75%-4%) has increased the cost of loans. Credit cards now average 21% interest, and mortgages are near 7.5%.

This environment is squeezing big purchases. For example, auto loan delinquencies (people missing car payments) hit 4.1%, the highest level since 2022.

The “K-Shaped” Economy Breaking it down by income shows a stark divide, often called a “K-shaped” economy.

- Low Earners (under $15K): Most pessimistic. They are battered by “sticky” prices on essentials like groceries (up 2.5%).

- Middle-Income ($50K-$100K): struggling with housing costs. Rent and mortgages now eat up 30% of their budgets.

- High Earners (over $100K): Still resilient. Buoyed by stock market gains, they are driving 40% of all spending.

For households, this means tighter belts. Plans to buy durable goods (like appliances) dropped by 10%. At Market World, we see this as a call to action: monitor these numbers monthly to protect your wallet.

Retail Sales Performance: What This Year’s Numbers Tell Us

Retail sales in 2025 tell a tale of resilience mixed with caution. Total sales hit $733.3 billion in September. This is up 4.3% from last year—solid, but slower than the 5.7% growth we saw in 2024.

However, when you adjust for inflation (price hikes), “real” growth is only 1.3%. This exposes the truth: people are spending more money to get fewer items.

Holiday Shopping Trends:

- Black Friday: Online sales soared to $11.8 billion (up 9.1%).

- In-Store Traffic: Dipped by 3.6%. People avoided physical stores.

- Cyber Monday: Smashed records at $14.25 billion.

- Buy-Now-Pay-Later (BNPL): Usage hit $1 billion (up 11%) as shoppers needed help stretching their budgets.

Winners vs. Losers:

- 📈 Winners: Electronics (up 7.2% thanks to new AI gadgets), Groceries (steady at 3%), and E-commerce (up 11%).

- 📉 Losers: Furniture (down 2.1% as high rates stop home upgrades), Apparel (down 1.5%), and Toys (flat).

The takeaway? Core retail (sales excluding gas and cars) grew just 1.9%, half the pace of last year. Consumers are “trading down”—buying store brands instead of premium ones. Since consumer spending makes up nearly 70% of the economy, this slowdown drags overall growth down.

2025 Q4 Recap vs 2024 Q4: A Year-over-Year Comparison

Q4 2025 capped a turbulent year, with consumer sentiment and retail sales showing directional shifts from 2024’s post-holiday rebound. Shutdown delays pushed October data to December releases, but early indicators paint a clearer picture: growth slowed, caution reigned, yet online resilience buffered the blow. Businesses eyeing inventory, individuals prepping budgets, and enterprises modeling demand cycles—here’s the breakdown.

Consumer Sentiment — Q4 2025 vs Q4 2024

Confidence is lower: Michigan index averaged 52 in Q4 2025 (vs. 68 in 2024), Conference Board at 89 (vs. 102). The shutdown’s shadow loomed large, dropping expectations 8.6 points in November alone. Interest rates, steady at 3.75%-4% post-October cut, cooled inflation to 3% but kept borrowing pricey—mortgage apps down 15% YoY. Inflation easing (CPI at 3.0% in September) offered relief, but “sticky” sectors like shelter (up 4%) fueled doubts.

The job market stabilized late-year: unemployment at 4.4% (up from 4.1% in 2024 Q4), but claims hit three-year lows at 191K in late November. Hiring slowed (119K jobs in September), yet low layoffs signal “no-hire, no-fire.” Future income expectations? Down 10%, with 30% citing wage stagnation amid 1.2% real growth. High earners bucked the trend, up 5% on stock highs, but overall, sentiment signals recession fears—worse than 2024’s optimism.

Retail Sales — Q4 2025 vs Q4 2024

Q4 2025 ended a turbulent year. Growth slowed and caution reigned, though online shopping saved the day. Here is the breakdown of the changes.

Consumer Sentiment — Q4 2025 vs Q4 2024

- Confidence is lower: The Michigan index averaged 52 this quarter, compared to 68 last year.

- Interest Rates: Rates held steady at roughly 3.75%-4%. This cooled inflation to 3% but kept borrowing expensive. Mortgage applications dropped 15%.

- Jobs: The market stabilized late in the year. Unemployment is at 4.4% (up from 4.1% last year). Hiring has slowed, but layoffs are also low—a trend we call “no-hire, no-fire.”

Retail Sales — Q4 2025 vs Q4 2024

- Spending Patterns: Sales grew 3.9% nominally (before inflation), compared to 4.5% in 2024.

- Less Stuff: While total sales rose, the actual number of units sold fell by 3%. Consumers bought less but paid more.

- Behavior Shift: Spending on necessities (groceries, health) rose 4%, while luxury spending fell 2%.

- Online Shift: E-commerce now claims 24.6% of total sales, up from 22% last year.

Actionable Insights:

- ➡ Businesses: Adjust your inventory. Stock 20% more essentials and cut discretionary (fun/luxury) items by 15%.

- ➡ Individuals: Brace for price swings. Lock in deals now, as tariffs could raise prices in 2026.

➡ Large Enterprises: Monitor sentiment weekly. Pivot investment toward e-commerce.

Key Economic Forces Driving Sentiment and Sales in 2025

Macro forces reshaped the economy this year. Here is how the major factors played out:

Inflation Trends & Price Stability Inflation cooled to 3.0% in September. This is better than mid-year, but “sticky” prices remain. Shelter (housing) costs are up 3.4%. For low and middle earners, this takes a 5-7% bite out of their budget for basics.

Interest Rates & Borrowing Costs The Fed cut rates slightly in October, but paused in December. With auto loans at 8.5% and credit cards at 21%, delinquencies (missed payments) represent a 20% increase year-over-year.

Job Market Cooling but Still Strong Unemployment is at 4.4%. The economy added 119K jobs in September, which is below the trend. However, wage growth is holding at 3.2%.

Global Events & Supply Chains Energy prices eased, but tariffs (taxes on imports) hiked the cost of goods by 2-3%. Geopolitical tensions added uncertainty to inflation forecasts.

What Shifting Consumer Behavior Means for Businesses

2025’s consumers are savvy savers. They are trading down in categories like clothing and using payment plans for 11% of holiday buys. Here is how to adapt:

Individuals In a high-cost world, budgeting is key. Use the 50/30/20 rule (50% needs, 30% wants, 20% savings). January and July will offer the best discounts for post-holiday clearances.

Small & Medium Businesses Use sentiment data to guide inventory. If sentiment scores are low, cut luxury stock by 10-20% and focus on “value packs.” Target value-drivers: 60% of shoppers are looking for “affordable quality.”

Large Corporations Integrate sentiment data into your AI models to improve forecasting accuracy. Marketing should focus heavily on e-commerce, as digital investment offers a much higher return on investment than physical stores.

2025 Outlook: What to Expect in the Coming Quarters

What is next? The vibe is cautiously optimistic.

- Spending: Consumers may spend 2.9% more in 2026, though tariffs will eat into real growth.

- Inflation: Expected to dip to 2.6%.

- Growth Sectors: Look for growth in AI devices (up 12%), services (5%), and home improvement (4%).

- Recession Risk: There is a 30% chance of recession, compared to a 70% chance of a “soft landing.” Watch job data closely.

Conclusion

Consumer sentiment and retail sales in 2025 paint a picture of cautious spending and uneven confidence. The economy is stabilizing after a year of high rates and inflation, but most households remain selective.

For businesses, the key takeaway is simple: understand that customers are prioritizing essentials. Adjust inventory and sales expectations accordingly. For individuals, use these indicators to make better financial decisions—from timing purchases to managing debt.

If you’d like to read more in-depth analysis, weekly economic updates, and actionable insights tailored for individuals and businesses worldwide, visit MarketWorld.com today.

FAQ

What is the current U.S. consumer sentiment index in late 2025?

The University of Michigan index is around 53.3 in December. This is near historic lows. The Conference Board index sits at 88.7, down 7% from last year.

How did Black Friday 2025 retail sales compare to 2024?

Online sales were strong, hitting $11.8B (up 9.1%). However, in-store traffic fell 3.6%. The total number of items sold dropped 3%, showing people are buying less volume.

Will inflation continue to cool in 2026?

Forecasts say yes, dipping to 2.6%.

However, new tariffs could add 0.5-1% to that number, keeping prices higher than preferred.

How does consumer confidence differ by income in 2025?

It is a “K-shaped” split. High earners (> $100K) are resilient with a score of 105. Middle incomes ($50K-$100K) are squeezed at 85. Low earners (< $15K) are struggling at 75.

What’s the outlook for U.S. retail sales in 2026?

Expect 3-4% growth to reach $7.2 trillion. E-commerce will take a larger share (18%).

Why track retail sales for GDP impact?

Consumer spending makes up 70% of the US GDP. A 1% dip in sales reduces national economic growth by roughly 0.7%.

{kind=link}